Do you or a loved one rely on Medicare for healthcare coverage? If so, it’s important to understand the Medicare donut hole. This coverage gap can leave you vulnerable to high out-of-pocket expenses.

In this article, we’ll break down what the donut hole is and how you can avoid it. We’ll also discuss how to exit the gap and answer common questions about reducing costs.

So if you’re looking for more information on the Medicare donut hole, read on!

Key Takeaways

- The Medicare Part D coverage includes four stages: deductible, initial coverage, coverage gap (the “donut hole”), and catastrophic coverage.

- During the coverage gap, patients must pay out-of-pocket for all drug costs, including brand-name and generic drugs, until reaching the catastrophic coverage stage.

- Eligible prescription drug assistance programs, medication therapy management (MTM) services, and discounts on brand-name drugs purchased while in the gap period can help lower medication costs.

- To avoid the donut hole, it’s important to understand the three phases of Medicare Part D, calculate annual spending limits, consider lower-cost alternatives, get one 90-day supply instead of three 30-day supplies, and ask doctors or pharmacists about generic or over-the-counter options.

- Review your overall drug cost with ArcticMeds.com and reduce insurance payments by taking advantage of their low prices.

What is the Medicare Donut Hole?

You may have heard of the dreaded “Medicare Donut Hole,” but do you know what it is?

The Medicare Donut Hole is a gap in the coverage provided by some Medicare prescription drug plans. It occurs after you and your plan have spent a certain amount for covered drugs, but before you reach the catastrophic coverage stage.

During this period, you are responsible for paying all of your drug costs out-of-pocket – including both brand-name and generic drugs. The exact point at which you enter the donut hole varies depending on your specific plan, as does the amount of money that must be spent before reaching the catastrophic coverage stage.

Once you’re in the donut hole, there are still ways to reduce your out-of-pocket costs. For example, many plans offer discounts on brand-name drugs purchased in this gap period. Additionally, some plans provide partial coinsurance payments during this time frame to help lower pocket costs even further when buying generic medications.

Although entering into the Medicare Donut Hole can be daunting, understanding how it works and taking advantage of available savings opportunities can help minimize its impact on your wallet.

Coverage Stages Overview

You’re not alone in feeling overwhelmed by the coverage stages of this prescription drug plan – let’s break it down together.

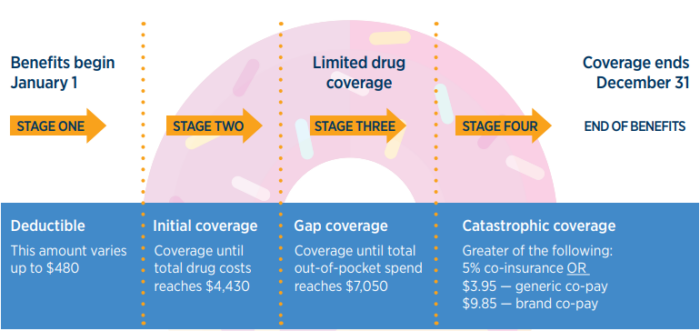

Medicare Part D provides prescription drug coverage and helps pay for covered drugs. The plan includes four stages: deductible, initial coverage, coverage gap (the “donut hole”), and catastrophic coverage.

During the deductible stage, you must pay out-of-pocket costs up to a certain limit before your insurance kicks in and pays part of your prescription drug costs.

After that, you enter into the initial coverage stage where your insurer pays a majority of your prescription drug costs until you reach an annual income set by the government.

This is when you enter into the donut hole or coverage gap; during this time, you are only responsible for a portion of your total prescription drug cost.

Finally, once you have reached a certain limit based on income level, you enter into the catastrophic coverage stage which requires minimal out-of-pocket costs at pharmacies for all covered drugs.

How to Avoid the Donut Hole

Navigating the prescription drug plan can be like walking a tightrope, but there are ways to keep from falling into the dreaded coverage gap.

To avoid entering the donut hole, it’s important to understand the three phases of Medicare Part D: the initial coverage stage, the coverage gap stage, and the catastrophic coverage phase.

In the initial phase, you’ll pay a monthly premium along with your deductible and co-pays for your drugs. Once you reach a certain threshold, usually around $4,020 in total drug costs (including both what you and your plan have paid), you enter the coverage gap or donut hole stage.

During this period, you’re responsible for paying 45% of brand-name drugs and 41% of generic drugs out-of-pocket until your total out-of-pocket spending reaches $6,350 (or $8,550 if you qualify for the low-income subsidy).

After that point is reached – which signals entry into the catastrophic coverage phase – you’ll only pay 5% or less of all remaining drug costs plus an additional pharmacy dispensing fee each time a drug is filled.

By staying aware of these stages and thresholds, it’s possible to avoid entering that dreaded donut hole altogether!

Review Your Overall Drug Costs and Avoid the Medicare Donut Hole

We work with patients every day to help them save money and maximize their insurance coverage. Follow this List and save even more money than ever on your drug costs:

- Contact ArcticMeds and get a quote on all of your medications.

- Then review the drugs covered by insurance vs the cost with us.

- Continue to purchase the highest price drugs with the most coverage through your insurance.

- Choose the medications with the lowest coverage and purchase from ArcticMeds.

The strategy here is by purchasing the drugs with the least coverage you will avoid the donut hole, keep coverage on your highest-priced drugs and end up paying less out of pocket than if you entered the donut hole.

If you manage the split effectively you will never enter the Medicare donut hole.

Exiting the Coverage Gap

Once you’ve reached the threshold of total out-of-pocket spending, you’ll be off the hook for most drug costs and back on solid ground.

Exiting the coverage gap, also known as the Medicare donut hole, means that your insurance plan will cover a certain portion of your pocket drug costs.

This is true when you reach the catastrophic coverage stage after meeting your annual deductible and reaching a subsidy that applies to your supply of prescription drugs.

The cost of prescription drugs is still expensive during this stage, so it’s important to keep track of any pocket expenses toward meeting that threshold and exiting the coverage gap.

After which, you can receive full benefits from your insurance plan for prescription drugs.

Common Questions Answered

Are you confused about how the coverage gap works and what it means for your prescription drug costs? Don’t worry – with a little research, you can be back in control of your healthcare.

The infamous donut hole or coverage gap is one aspect of Medicare Part D that affects millions of non-LIS enrollees. It’s important to understand the different drug tiers, copays, deductibles, and coinsurance costs associated with this level of insurance called Medicare Part D.

For instance, generic medications have lower copays than brand-name medications and many plans offer discounts from drug manufacturers to help offset some of the cost of drugs.

This also includes eligible prescription drug assistance programs designed to bring down medication costs by providing choices between medications or offering alternatives, such as lower-cost drugs.

Additionally, there are yearly limits on what you pay out-of-pocket for covered insulin drugs as well as costly breakthrough medications. Some providers may also provide medication therapy management (MTM) services, which can help you find the right list of medications that work best for you — all while keeping an eye on your medication option’s cost.

Understanding how the coverage gap works is essential when considering all plan premiums and benefit levels associated with your plan.

Depending on where in the three stages — initial coverage phase; coverage gap phase; catastrophic payment stage — you fall will determine your pocket limit and share of costs responsibilities associated with covered prescriptions drugs and pharmacies in their network.

Ultimately it’s up to each policyholder to calculate their annual spending limit based on their deductible phase followed by coinsurance costs once reaching their pocket threshold or annual coverage limit before reaching catastrophic coverage limit.

This is when Medicare pays for 95% of a beneficiary’s drug expenses after they’ve spent approximately $6,350 out-of-pocket in a single year within their plan premium and discounts from drug manufacturers combined!

Reducing Costs in the Gap

Making sense of the coverage gap doesn’t have to be a struggle – with a few smart moves, you can get your healthcare costs back under control.

The ‘Medicare donut hole’, as it’s commonly referred to, occurs when an enrollee’s total drug cost, including copayments and discounts from their Medicare Part D plan, reaches the initial coverage limit set by the federal government.

Once that happens, enrollees are responsible for paying a larger share of their prescription medications until they reach the catastrophic coverage level.

To help ease this burden on those with limited incomes or resources, there’s an income-based assistance program called Extra Help that helps eligible individuals pay for the entire cost of their prescription benefits.

Another way to reduce costs in the gap is to check if drug companies offer lower-cost alternatives approved by the Federal Drug Administration (FDA).

A person can also save money on prescription drugs by getting one 90-day supply instead of three 30-day supplies; this will help avoid multiple copays throughout the period.

Finally, asking your doctor or pharmacist about generic or over-the-counter options could provide additional savings during this time too.

By taking advantage of these strategies while in the donut hole period, enrollees can save more money with Medicare and Social Security funds and better manage their medical expenses overall.

Frequently Asked Questions

How long does the donut hole coverage last?

Your coverage in the donut hole won’t last forever! It’s surprisingly short-lived – typically just lasting a few months. But don’t worry, once you’ve reached the other side of the Medicare donut hole, your Medicare Part D plan will kick back in to save the day!

Are there any alternatives to the donut hole coverage?

Yes, there are alternatives to the donut hole coverage. Medicare Advantage plans and other private insurance may offer additional benefits or lower costs than traditional Medicare. Speak with your doctor or insurance provider for more information.

What are the qualifications to be eligible for the donut hole coverage?

Do you want to be eligible for donut hole coverage? Well, let me tell you a story that might help. You need to be enrolled in Medicare Part A and B and must have spent a certain amount on prescriptions in the current coverage period to qualify.

What is the maximum amount I can save by using the donut hole coverage?

You can save up to $3,820 in out-of-pocket costs with donut hole coverage. This includes discounts on brand-name and generic drugs.

Are there any other expenses associated with the donut hole coverage?

You may need to pay more out-of-pocket for brand-name drugs while in the donut hole coverage. Additionally, you may need to pay a deductible or coinsurance on generic and brand-name drugs. Rhetorically speaking, this could be a costly experience if you are not prepared.

Conclusion

You’ve come to the end of your journey learning about the Medicare Donut Hole. It’s a complex and tricky landscape, but with knowledge comes power.

Think of it like a puzzle – each piece is important to understanding how it works and how you can best prepare for it.

You now have the tools to make informed decisions on how to reduce costs in this coverage gap. As long as you stay diligent and keep an eye out for changes, you’ll be able to navigate through the donut hole like a pro!